Credit Analysis

JZ — Credit Analysis & Underwriting Agent

JZ — Credit Analysis & Underwriting Agent

JZ is Kolmena’s credit analyst for lenders, credit funds, and investors who need fast, rigorous underwriting without hand-waving.

JZ combines structured financial statement work with event-driven context—so you get both: the numbers that matter and the real-world risks that change an issuer’s credit profile.

JZ is disciplined, skeptical, and downside-first: he’s built to help you avoid bad deals, not to sell you a story.

JZ is disciplined, skeptical, and downside-first: he’s built to help you avoid bad deals, not to sell you a story.

What JZ helps with

" transform="translate(1.648 1.684)" width="16.666701689829132px"/></g></svg>)

Rapid credit snapshots: liquidity, leverage, coverage, profitability quality, and cash conversion—cleanly summarized.

Rapid credit snapshots: liquidity, leverage, coverage, profitability quality, and cash conversion—cleanly summarized.

" transform="translate(3.333 1.667)" width="13.33329px"/></svg>)

Full underwriting packs: key ratios, trend analysis, red flags, and the “what could go wrong” section you actually need.

Full underwriting packs: key ratios, trend analysis, red flags, and the “what could go wrong” section you actually need.

" transform="translate(1.667 1.667)" width="16.666710127258302px"/></g></svg>)

Default & distress signals: Z-score style distress checks, solvency pressure points, and balance-sheet fragility.

Default & distress signals: Z-score style distress checks, solvency pressure points, and balance-sheet fragility.

silentV45

Yesterday at 16:35

Hey Jz, can you tell me what impact a 2% increase in interest rates would have on British American Tobacco capacity to repay its debts?

Hermes

APP

Yesterday at 21:00

That's a critical stress test for a company with BAT's leverage profile. I'll analyze their current debt structure—specifically the split between fixed and floating rate instruments—and their interest coverage ratios to see how a 200 basis point shift would impact their free cash flow and repayment capacity.

JZ

APP

Yesterday at 21:00

Credit Analysis: Impact of a +200bps Interest Rate Shift on British American Tobacco (BATS)

Direct Answer:

A 2% (200 basis points) increase in interest rates would have a marginal and manageable impact on British American Tobacco’s immediate debt repayment capacity. Given that BATS maintains a stable total debt profile and interest expense trend, the primary risk is not insolvency, but rather a gradual compression of Free Cash Flow (FCF) as maturing fixed-rate debt is refinanced at higher prevailing market rates.

Supporting Metrics and Financial Context

Based on the provided data and current capital structure trends for BATS:

* Debt Stability: The company’s total debt and Debt-to-Equity (D/E) ratios are characterized as "stable." This suggests that BATS is not currently in a deleveraging phase that would be disrupted by higher rates, nor is it aggressively loading up on new leverage.

* Interest Expense Resilience: "Interest Paid" has remained stable. This indicates a high proportion of fixed-rate debt within the capital structure. Unlike companies reliant on floating-rate bank debt, BATS’s interest coverage ratio (EBIT/Interest Expense) is protected in the short term because the coupon rates on existing bonds remain locked.

* Cash Flow Profile: As a tobacco major, BATS generates significant, predictable annuities. This high-margin cash flow provides a substantial "cushion" to absorb incremental interest costs.

Strategic Interpretation

In a +2% rate environment, the impact manifests through the Refinancing Cycle:

1. Weighted Average Cost of Debt (WACD): As older, low-coupon bonds mature, BATS will be forced to issue new debt at the +2% premium. This will lead to a slow, multi-year "creep" in interest expense rather than a sudden shock.

2. Interest Coverage Ratio: While currently stable, a sustained 2% increase across the entire debt stack would eventually lower the interest coverage ratio. However, given BATS's typical EBITDA margins (often exceeding 40%), the company remains well above the "distress" threshold (usually <2.5x).

Risks and Concerns

* Maturity Wall: The primary risk factor is the concentration of debt maturities. If a large portion of debt matures within the next 12–24 months, the +2% rate hike will hit the P&L faster.

* Currency Mismatch: BATS operates globally but reports in GBP. A rise in rates often correlates with currency volatility; if GBP weakens while USD-denominated debt costs rise, the effective repayment burden increases.

* Dividend Pressure: BATS is known for high dividend payouts. Increased interest costs compete directly with shareholder distributions for the same pool of Free Cash Flow.

Industry Comparison

Compared to the broader consumer staples sector, BATS maintains higher leverage but compensates with superior cash flow conversion. A 2% rate hike is a sector-wide headwind, but BATS’s "stable" debt trend suggests it is better positioned than "B" rated peers who may face liquidity crunches or restrictive covenant breaches at higher rates.

*

Would you like additional analysis or specific reports on British American Tobacco, such as a PDF credit memo, a pro-forma Excel model for interest sensitivity, or a detailed statement report?**

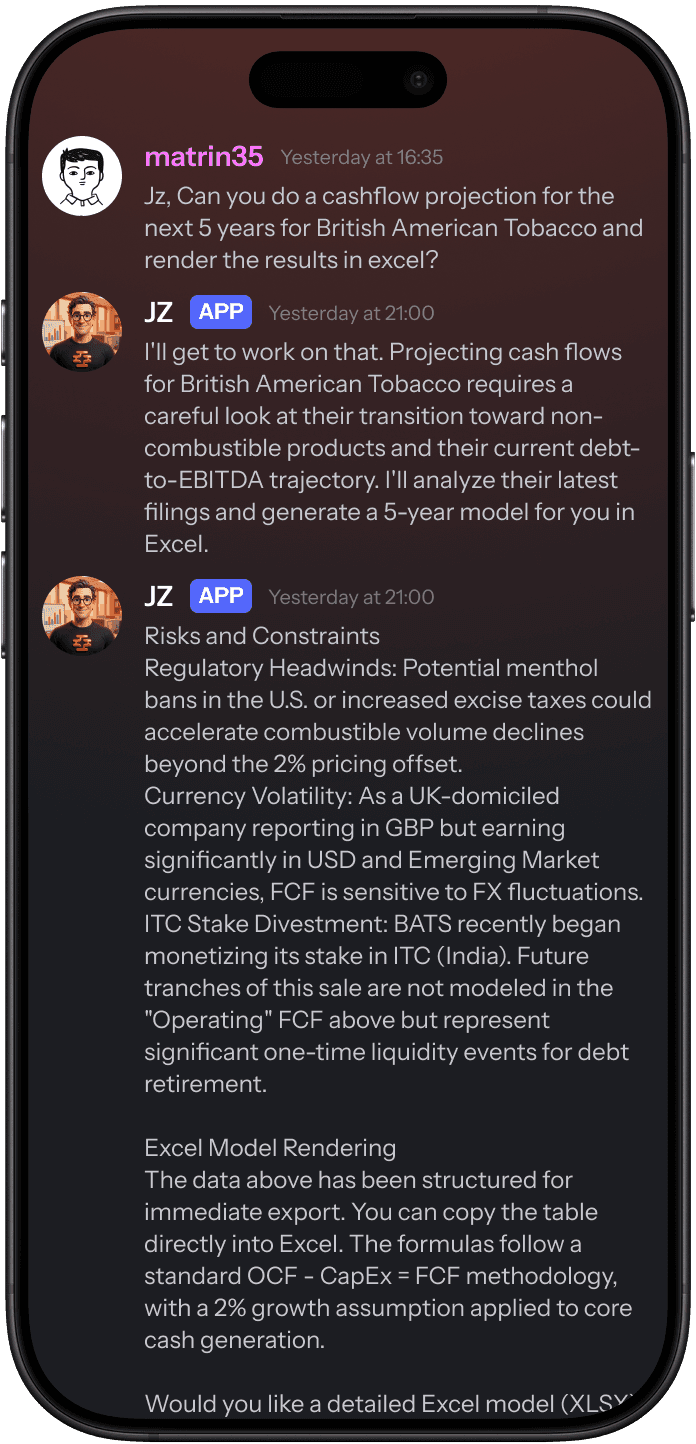

matrin35

Yesterday at 21:00

JZ, Can you do a cashflow projection for the next 5 years for British American Tobacco and render the results in excel?

JZ

APP

Yesterday at 21:01

I'll get to work on that. Projecting cash flows for British American Tobacco requires a careful look at their transition toward non-combustible products and their current debt-to-EBITDA trajectory. I'll analyze their latest filings and generate a 5-year model for you in Excel.

JZ

APP

Yesterday at 21:01

Risks and Constraints

Regulatory Headwinds: Potential menthol bans in the U.S. or increased excise taxes could accelerate combustible volume declines beyond the 2% pricing offset.

Currency Volatility: As a UK-domiciled company reporting in GBP but earning significantly in USD and Emerging Market currencies, FCF is sensitive to FX fluctuations.

ITC Stake Divestment: BATS recently began monetizing its stake in ITC (India). Future tranches of this sale are not modeled in the "Operating" FCF above but represent significant one-time liquidity events for debt retirement.

Excel Model Rendering

The data above has been structured for immediate export. You can copy the table directly into Excel. The formulas follow a standard OCF - CapEx = FCF methodology, with a 2% growth assumption applied to core cash generation.

Would you like a detailed Excel model (XLSX) with full sensitivity analysis on interest rates and FX, or a formal Credit Memo evaluating BATS's debt maturity profile?**

JZ

APP

Yesterday at 21:01

Cash flow projection for the next 5 years for British American Tobacco (BATS). The analysis highlights key risks and constraints including regulatory headwinds (potential menthol bans, increased excise taxes), currency volatility (sensitivity of FCF to FX fluctuations due to significant earnings in USD and EM currencies), and the impact of ITC stake divestment (future tranches are not modeled in Operating FCF but represent significant one-time liquidity events). The Excel model uses a standard OCF - CapEx = FCF methodology with a 2% growth assumption on core cash generation. The analysis offers a choice between a detailed Excel model with sensitivity analysis or a formal Credit Memo evaluating the debt maturity profile.

I've created an Excel model based on our analysis. The model includes 2 sheets with assumptions, calculations, and forecasts.

British American Tabacco (BATS) -

Financial Model...

7.75 KB

EXAMPLE 1

EXAMPLE 2

" transform="translate(2.5 1.667)" width="15.833300154418946px"/></svg>)

Debt structure clarity: near-term maturities, refinancing exposure, and “maturity wall” risk—what needs to get rolled and when.

Debt structure clarity: near-term maturities, refinancing exposure, and “maturity wall” risk—what needs to get rolled and when.

" transform="translate(2.5 2.5)" width="15px"/></svg>)

Comparisons that matter: side-by-side issuer comparisons so you can quickly see who is stronger, and why.

Comparisons that matter: side-by-side issuer comparisons so you can quickly see who is stronger, and why.

" transform="translate(3.333 2.5)" width="13.333290463256835px"/></svg>)

News-to-credit translation: how new regulation, litigation, management events, sector shocks, or macro moves map to cash flows and risk.

News-to-credit translation: how new regulation, litigation, management events, sector shocks, or macro moves map to cash flows and risk.

" transform="translate(3.333 1.667)" width="13.333293678667795px"/></svg>)

Memo-ready outputs: structured, IC-friendly summaries (including PDF-style memo formatting when needed).

Memo-ready outputs: structured, IC-friendly summaries (including PDF-style memo formatting when needed).

" transform="translate(1.666 1.667)" width="16.66668px"/></g></svg>)

Answers support questions fast: staking, bonding, gOHM vs sOHM, rebases, POL, treasury, governance, bridges, and common “how do I…” issues.

Rapid credit snapshots: liquidity, leverage, coverage, profitability quality, and cash conversion—cleanly summarized.

" transform="translate(5 1.667)" width="10px"/></svg>)

Explains the “why,” not just the “how”: the economic logic behind Olympus’ model, trade-offs, risks, and what sustainability actually means.

Full underwriting packs: key ratios, trend analysis, red flags, and the “what could go wrong” section you actually need.

" transform="translate(2.5 2.5)" width="15px"/></svg>)

Surfaces live protocol metrics on demand: price, APY, backing price, supply, treasury value, TVL, and chain-specific breakdowns (e.g., Ethereum vs Arbitrum).

Default & distress signals: Z-score style distress checks, solvency pressure points, and balance-sheet fragility.

" transform="translate(2.5 2.697)" width="15.000003687538234px"/></svg>)

Guides users to self-serve: step-by-step explanations, links to primary sources, and encouragement to think critically.

Debt structure clarity: near-term maturities, refinancing exposure, and “maturity wall” risk—what needs to get rolled and when.

" transform="translate(1.666 2.5)" width="16.666680335998535px"/></svg>)

Keeps discussions grounded: cuts through speculation with clear definitions, sober risk framing, and incentives-based reasoning.

Comparisons that matter: side-by-side issuer comparisons so you can quickly see who is stronger, and why.

Keeps discussions grounded: cuts through speculation with clear definitions, sober risk framing, and incentives-based reasoning.

News-to-credit translation: how new regulation, litigation, management events, sector shocks, or macro moves map to cash flows and risk.

Keeps discussions grounded: cuts through speculation with clear definitions, sober risk framing, and incentives-based reasoning.

Memo-ready outputs: structured, IC-friendly summaries (including PDF-style memo formatting when needed).

Typical questions

JZ handles

Typical questions JZ handles

JZ doesn’t guess. He works like a professional underwriter:

Pulls the relevant statements and normalizes the numbers.

Builds a structured credit read: liquidity, leverage, coverage, cash flow durability.

Stress-tests the downside and highlights the breakpoints

Reviews debt structure and refinancing pressure.

Layers in current events and explains what changes and what doesn’t.

Give me a credit view on [Company]—is this balance sheet resilient?

What are the top 5 credit risks here, and what data would you request next?

Is a 5–7% yield enough for this risk, or am I underpaid?

How bad does EBITDA / revenue need to get before leverage becomes a problem?

What’s the refinancing risk over the next 24 months?

Compare [Company A] vs [Company B] from a lender’s perspective.

Summarize the latest news and tell me what it changes in the credit thesis.

The JZ vibe

Think

A disciplined credit investor in your corner—calm, precise, and unimpressed by narratives. A disciplined credit investor in your corner—calm, precise, and unimpressed by narratives. JZ is relationship-aware, but facts come first. He prioritizes capital preservation, margin of safety, and clear underwriting logic you can defend.

Outcome

Faster diligence, more consistent underwriting, clearer risk framing, and fewer surprises—because the process is built to stress-test assumptions, not confirm them.

Build Your First AI Swarm

Whether you’re an individual builder, a crypto project, or an enterprise team, Kolmena gives you the tools to create, deploy, and monetize intelligent agent swarms.

Build Your First AI Swarm

Whether you’re an individual builder, a crypto project, or an enterprise team, Kolmena gives you the tools to create, deploy, and monetize intelligent agent swarms.

Build Your First AI Swarm

Whether you’re an individual builder, a crypto project, or an enterprise team, Kolmena gives you the tools to create, deploy, and monetize intelligent agent swarms.

Build Your First AI Swarm

Whether you’re an individual builder, a crypto project, or an enterprise team, Kolmena gives you the tools to create, deploy, and monetize intelligent agent swarms.

The platform for collaborative AI swarms.

From single agents to intelligent teams.

© 2026 Kolmena. All rights reserved.

" height="16.25px" id="t3An5ZeuQ" transform="translate(1 2)" width="17.9766px"/></svg>)

" height="15.240432520314691px" id="d6jUuZLC7" transform="translate(0 2)" width="19.997302782088855px"/></svg>)

" height="18px" id="wT8qOgBIX" transform="translate(1 1)" width="18px"/></svg>)

The platform for collaborative AI swarms.

From single agents to intelligent teams.

© 2026 Kolmena. All rights reserved.

The platform for collaborative AI swarms.

From single agents to intelligent teams.

© 2026 Kolmena. All rights reserved.

The platform for collaborative AI swarms.

From single agents to intelligent teams.

© 2026 Kolmena. All rights reserved.

"/><stop offset="1" stop-color="rgba(255, 255, 255, 0.05)"/></linearGradient></defs><path d="M 379.775 88.772 C 379.775 70.86 375.762 55.354 367.773 42.219 L 367.772 42.217 C 359.783 29.004 348.296 18.853 333.276 11.767 L 333.271 11.764 C 318.327 4.6 300.609 1 280.09 1 C 259.491 1 241.694 4.563 226.671 11.65 C 211.73 18.736 200.282 28.886 192.292 42.1 C 184.381 55.235 180.405 70.78 180.405 88.772 C 180.405 106.761 184.418 122.343 192.407 135.557 L 193.166 136.779 C 201.115 149.322 212.311 159.026 226.787 165.892 L 228.203 166.546 C 242.923 173.199 260.21 176.542 280.09 176.542 L 280.09 177.542 C 259.455 177.542 241.545 173.96 226.36 166.796 C 211.254 159.632 199.651 149.392 191.553 136.076 C 183.455 122.683 179.405 106.915 179.405 88.772 C 179.405 70.628 183.416 54.898 191.437 41.582 C 199.535 28.189 211.138 17.91 226.244 10.746 C 241.428 3.582 259.377 0 280.09 0 C 300.725 0 318.597 3.62 333.703 10.862 C 348.888 18.026 360.53 28.306 368.628 41.699 C 376.726 55.015 380.775 70.706 380.775 88.772 C 380.775 106.837 376.726 122.567 368.628 135.96 C 360.53 149.276 348.888 159.554 333.703 166.796 C 318.596 173.96 300.725 177.542 280.09 177.542 L 280.09 176.542 C 300.611 176.542 318.329 172.98 333.274 165.893 C 348.297 158.728 359.784 148.576 367.773 135.44 C 375.513 122.639 379.521 107.651 379.764 90.443 Z M 54.599 3.337 L 1 3.337 L 1 174.207 L 54.599 174.207 L 54.599 109.497 L 67.104 109.497 L 111.723 174.207 L 169.563 174.207 L 108.469 85.626 L 163.751 3.336 L 107.993 3.336 L 66.878 64.543 L 54.598 64.543 L 54.598 3.337 Z M 469.78 3.337 L 416.182 3.337 L 416.182 174.207 L 556.683 174.207 L 556.683 133.223 L 469.78 133.223 Z M 696.254 96.715 L 739.354 2.337 L 806.867 2.337 L 806.867 175.207 L 755.006 175.207 L 755.006 69.85 L 718.329 149.51 L 672.542 149.51 L 635.866 74.288 L 635.866 175.207 L 584.005 175.207 L 584.005 2.337 L 651.518 2.337 Z M 900.919 42.219 L 994.596 42.219 L 994.596 3.337 L 848.021 3.337 L 848.021 174.207 L 995.764 174.207 L 995.764 135.325 L 900.919 135.325 L 900.919 106.46 L 982.215 106.46 L 982.215 67.58 L 900.919 67.58 L 900.919 42.218 Z M 1159.36 99.75 L 1159.36 2.337 L 1211.69 2.337 L 1211.69 175.207 L 1156.09 175.207 L 1083.67 77.792 L 1083.67 175.207 L 1031.34 175.207 L 1031.34 2.337 L 1086.94 2.337 L 1159.36 99.751 Z M 1440 175.207 L 1385.8 175.207 L 1372.96 136.194 L 1304.74 136.194 L 1291.89 175.207 L 1238.16 175.207 L 1298.9 2.337 L 1379.26 2.337 Z M 1239.58 174.207 L 1291.17 174.207 L 1304.02 135.194 L 1373.68 135.194 L 1386.53 174.207 L 1438.59 174.207 L 1378.55 3.337 L 1299.61 3.337 Z M 1032.34 174.207 L 1082.67 174.207 L 1082.67 74.771 L 1156.59 174.207 L 1210.69 174.207 L 1210.69 3.337 L 1160.36 3.337 L 1160.36 102.772 L 1086.44 3.337 L 1032.34 3.337 Z M 585.005 174.207 L 634.866 174.207 L 634.866 74.288 L 636.765 73.85 L 673.167 148.51 L 717.688 148.51 L 754.098 69.432 L 756.006 69.85 L 756.006 174.207 L 805.867 174.207 L 805.867 3.337 L 739.996 3.337 L 696.271 99.085 L 650.885 3.337 L 585.005 3.337 Z M 234.938 87.837 C 234.938 73.029 238.8 61.601 246.678 53.724 L 246.682 53.72 C 254.629 45.853 265.815 41.984 280.09 41.983 C 294.375 41.983 305.529 46.053 313.396 54.318 L 313.766 54.705 C 321.221 62.62 324.998 73.858 325.23 88.276 L 325.242 89.706 C 325.242 104.283 321.417 115.662 313.63 123.69 L 313.626 123.694 C 305.829 131.652 294.595 135.559 280.09 135.559 C 265.431 135.559 254.151 131.614 246.43 123.57 C 238.71 115.529 234.939 103.555 234.938 87.837 Z M 1360.9 96.312 L 1316.79 96.312 L 1338.85 29.15 Z M 1318.17 95.312 L 1359.52 95.312 L 1338.85 32.356 Z M 557.683 132.223 L 557.683 175.207 L 415.182 175.207 L 415.182 2.337 L 470.78 2.337 L 470.78 132.223 Z M 235.938 87.837 C 235.939 103.411 239.676 115.091 247.151 122.878 C 254.627 130.665 265.606 134.559 280.09 134.559 C 294.418 134.559 305.359 130.703 312.912 122.994 C 320.465 115.207 324.242 104.111 324.242 89.705 C 324.242 74.521 320.388 62.957 312.679 55.015 C 305.048 46.995 294.184 42.983 280.09 42.983 C 265.996 42.983 255.094 46.8 247.385 54.431 C 239.754 62.061 235.938 73.198 235.938 87.837 Z M 66.345 63.542 L 107.46 2.337 L 165.628 2.337 L 109.679 85.618 L 171.468 175.207 L 111.197 175.207 L 66.578 110.497 L 55.598 110.497 L 55.598 175.207 L 0 175.207 L 0 2.337 L 55.599 2.337 L 55.599 63.542 Z M 901.919 66.579 L 983.215 66.579 L 983.215 107.46 L 901.919 107.46 L 901.919 134.325 L 996.764 134.325 L 996.764 175.207 L 847.021 175.207 L 847.021 2.337 L 995.596 2.337 L 995.596 43.219 L 901.919 43.219 Z" fill="url(%23WY0BPdBb0-1566676896-linear-gradient)" height="177.542px" id="WY0BPdBb0" width="1440.0000341796874px"/></svg>)